Canada’s economy regains some footing

By BDC MONTREAL, Canada – For much of the past year, the Canadian economy has looked like a slow burn. Growth kept losing altitude, recession headlines kept resurfacing, and each new data release seemed to give entrepreneurs another reason to stay cautious. Luckily, spring brought a change in tone. Real GDP turned positive again in April, […] The post Canada’s economy regains some footing appeared first on Caribbean News Global.

By BDC

MONTREAL, Canada – For much of the past year, the Canadian economy has looked like a slow burn. Growth kept losing altitude, recession headlines kept resurfacing, and each new data release seemed to give entrepreneurs another reason to stay cautious. Luckily, spring brought a change in tone.

Real GDP turned positive again in April, Statistics Canada’s advance estimate pointed to another modest gain in May, employment continued to rise in June, and trade began to move in a more encouraging direction. The Canadian economy is not booming. The conflict in the Middle East, US tariffs, elevated energy prices and weak population growth are still shaping the backdrop. But the data now point to an economy that is regaining some footing rather than sliding deeper into weakness. BDC Economics is maintaining its 1.0 percent real GDP growth forecast for 2026.

The recovery the economy needed

Real GDP edged down by 0.1 percent at an annualised rate in the first quarter, after a contraction in late 2025. That weakness was concentrated in a few volatile components. Net trade was the main drag, as imports rose while export volumes remained soft, and government spending also pulled back after earlier strength. At the same time, household consumption continued to provide support, and inventories offset part of the weakness. The result was not an economy in free fall, but one operating below potential and struggling to find momentum.

April changed the tone. Real GDP grew 0.5 percent month over month, the strongest monthly gain in several months. The improvement was broad-based: 14 of 20 industries expanded, goods-producing industries rose 1.2 percent, and services grew 0.3 percent for a third consecutive month. Mining, quarrying, and oil and gas extraction led the gain with a 2.9 percent increase, reflecting the support coming from higher energy prices and stronger commodity activity.

May appears to have held the line as well. Statistics Canada’s advance estimate pointed to a further 0.1 percent increase. Taken together, the latest data suggest that second-quarter growth came in clearly positive. The Bank of Canada now estimates that GDP growth strengthened to about 2.5 percent annualized in Q2, supported by stronger exports, a partial rebound from temporary weakness in Q1 and firmer residential investment.

What makes this pickup more meaningful is the context in which it is happening. The headwinds have not disappeared. The conflict in the Middle East continues to create volatility in energy and food prices. Trade uncertainty remains elevated. US tariffs on metals and related products continue to weigh on trade-exposed industries. And the CUSMA review process is now adding an annual rolling layer of uncertainty for businesses. The improvement is real, but it is still fragile.

Trade is finally moving in the right direction

If one number explains why the first quarter looked so weak, it is the contribution from net trade. Rising imports and soft export volumes together subtracted roughly 3.8 percentage points from Q1 GDP growth, more than offsetting the positive contributions from household consumption and inventories.

The second-quarter picture looks materially better. Export volumes stabilised through the spring, with energy exports providing support, and the merchandise trade balance moved back toward surplus. Imports also continued to rise, which can be a drag on headline GDP. But not all imports tell the same story. A portion of machinery and equipment imports may point to businesses investing in capacity or retooling their operations, although it is too early to call this a broad investment rebound.

The key point is that trade is no longer deteriorating at the same pace. After being the main reason GDP weakened in Q1, trade should contribute more favourably to Q2 growth. That does not mean trade risks have disappeared. It means the economy is still adapting to them.

A historic demographic shift is now official

While the trade story is cautiously encouraging, the demographic story is more structural. Canada’s population declined for a third consecutive quarter at the start of Q2 2026, something unprecedented in modern Canadian demographic reporting. A historic decline in Canada’s population with significant consequences for the economy and businesses, and it is now firmly entrenched in the data.

The mechanics are straightforward, with the non-permanent residents estimate falling 4.4 percent in a single quarter and permanent immigrant inflows also dropped roughly 20 percent year over year.

The economic consequences are already visible. Population growth had been one of the biggest engines of Canadian expansion since 2022. More people meant more consumers, more renters and buyers, more workers, and more baseline demand across most sectors.

The bank of Canada previously estimated that newcomers added about 2.5 percent to potential output between late 2022 and early 2024. Reversing part of that flow inevitably changes the outlook. Fewer new residents mean less demand for consumer goods and services, fewer new households, and lower pressure on housing demand than in recent years. This does not mean housing weakness is only demographic. Interest rates, affordability and confidence still matter. But slower population growth now adds a structural layer to what had already been a cyclical cooling in housing activity.

For businesses, the implication is simple: growth will rely less on an expanding customer base and more on productivity, market share and efficiency.

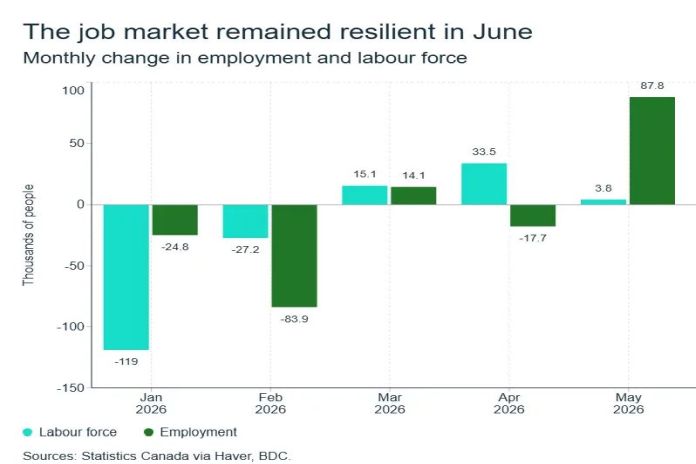

Jobs keep coming, but the labour market remains uneven

The June labour market data provided exactly the kind of confirmation the economy needed after a strong May. Employment rose by 18,000 in June, following May’s much larger gain of 87,800. That two-month combo has now clawed back most of the 112,000 jobs lost between January and April.

The unemployment rate slipped to 6.5 percent, down from 6.6 percent in May and 6.9 percent in April, while wage growth continued to firmed to 3.3 percent year over year. With population growth no longer expanding the labour force as rapidly as it did in recent years, even modest hiring can now push the unemployment rate lower. That does not mean the labour market is tight everywhere. It means the operating environment is changing.

The composition of the gains matters as much as the headline. Services sectors, especially accommodation, food services, and retail and wholesale trade, are still doing most of the heavy lifting, while manufacturing lost another 17,000 jobs in June. That is the clearest reminder that the recovery remains uneven. Domestic-facing sectors are stabilizing, but trade-exposed industries are still under pressure from tariffs and weak external demand.

What it means for entrepreneurs

- Do not expect a rate cut for 2026. With Q2 GDP tracking above 2 percent annualised, inflation firming on the back of higher energy prices, and unemployment drifting lower, there is little urgency for the Bank of Canada to move off its 2.25 percent policy rate, so plan financing decisions around a stable, not falling, rate through the summer (but check out this month main article for more details on interest rates).

- The second quarter looks clearly positive, which reduces the risk that the mild technical recession narrative turns into a broader downturn story. But growth remains below potential, and the economy is still operating with excess supply, plan accordingly.

- Demographics are now part of the business environment. Slower population growth means slower expansion in baseline demand. It also means labour supply will be less forgiving. Entrepreneurs should not assume that today’s softer labour market will last. Retention, training, automation and productivity investments are becoming more important, not less.

- Trade uncertainty is still the main wildcard. Exporters and manufacturers should continue to plan for uneven conditions, especially in sectors exposed to US tariffs now that CUSMA annual reviews are officials.

The post Canada’s economy regains some footing appeared first on Caribbean News Global.