Namibia, Niger and South Africa on global radar as France, China and Russia chase Africa’s uranium

Africa’s uranium industry is becoming a strategic front in the global race for nuclear fuel, as rising reactor demand, supply-security concerns and resource nationalism draw fresh attention to the continent’s reserves.

Africa’s uranium industry is becoming a strategic front in the global race for nuclear fuel, as rising reactor demand, supply-security concerns and resource nationalism draw fresh attention to the continent’s reserves.

- Africa is becoming increasingly significant in the global uranium industry due to growing nuclear reactor demand and geopolitical interest in nuclear fuel supply.

- Namibia, Niger, and South Africa are major uranium resource holders in Africa, with Namibia ranking third globally in production after Kazakhstan and Canada.

- Niger has become a center of resource nationalism, reducing foreign control, cancelling licenses, and shifting alliances, leading to output declines and geopolitical tensions.

- France, China, and Russia are competing for influence over African uranium resources, with China consolidating assets in Namibia and Russia showing interest in Niger and Tanzania projects.

Globally, Australia remained the clear leader in 2023, with 1.67 million tonnes of identified recoverable uranium, or 28% of the world total, according to OECD Nuclear Energy Agency and International Atomic Energy Agency data.

Kazakhstan followed with 813,900 tonnes and Canada with 582,000 tonnes, giving the three countries 52% of global identified resources.

Africa, however, holds several of the next major uranium resource bases, with Namibia ranking fourth globally at 497,900 tonnes, followed by Niger with 336,000 tonnes and South Africa with 320,900 tonnes.

Meanwhile, Namibia ranks even higher in production, standing as the world’s third-largest uranium producer after Kazakhstan and Canada after record output last year topped 10,000 tonnes of U3O8, commonly known as yellowcake.

Botswana, with 87,200 tonnes, and Tanzania, with 57,700 tonnes, add further depth to Africa’s long-term supply position.

Africa attracts fresh exploration capital

The OECD-NEA/IAEA Red Book put global uranium exploration and mine development spending at an expected $840 million in 2023, up 5% from 2022.

Africa’s share rose from 4% of reported global expenditure in 2020 to 12% in 2022, before easing to an estimated 9% in 2023.

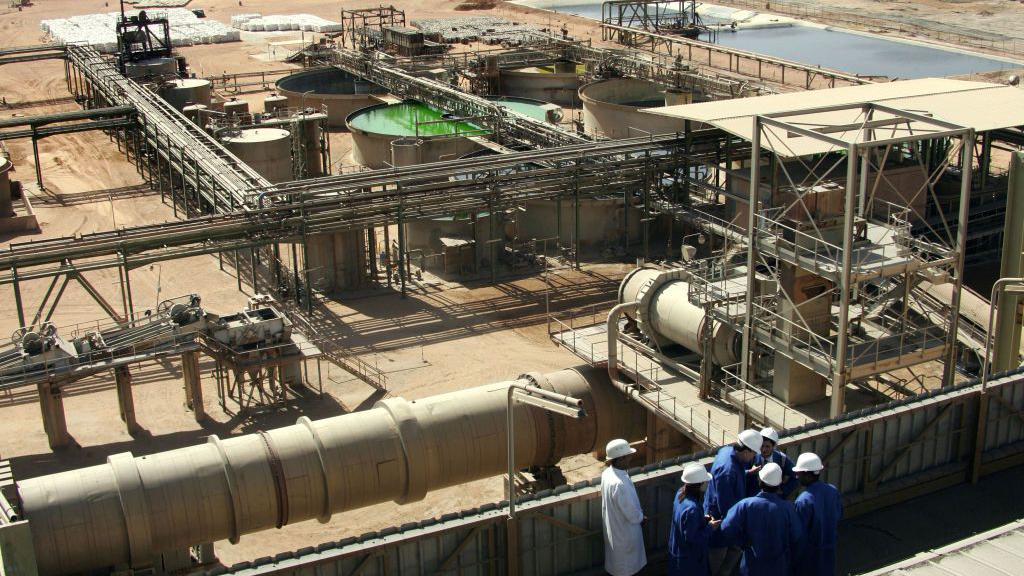

Namibia has drawn the largest share of African spending, with exploration and mine development expenditure rising from $11 million in 2020 to $86 million in 2022, before easing to an expected $75 million in 2023.

Over the same period, about 342,436 metres were drilled in the country, most of it linked to uranium exploration.

The country produced 5,754 tonnes of uranium in 2021 and 5,612 tonnes in 2022, before output rose 25% to 6,985 tonnes in 2023, driven by Husab and Rössing.

In 2024, it produced 7,333 tonnes, placing it behind only Kazakhstan and Canada among global producers, according to the World Nuclear Association.

By 2025 and early 2026, Namibia’s position had strengthened further, with Reuters reporting that uranium output rose 22% year on year in the first 10 months of 2025 while as Paladin Energy moved to ramp up Langer Heinrich.

The company says the mine is on track to reach maximum output from July 2026.

That production base has also become geopolitically important because much of Namibia’s uranium industry is tied to major foreign players.

Husab is operated by Swakop Uranium, backed by China General Nuclear Power Group, while Rössing is controlled by China National Uranium Corp.

Meanwhile, Deep Yellow’s Tumas and Bannerman Energy’s Etango projects remain part of Namibia’s next development wave.

Niger shifts from supplier to risk centre

By contrast, Niger remains one of Africa’s established uranium producers, as it reshapes the sector around greater domestic control and long-term project development.

Niger’s uranium output fell from 2,248 tonnes in 2021, produced from Arlit and Akouta, to 2,020 tonnes in 2022, all from Arlit, after Cominak shut the Akouta mine in March 2021 following more than 40 years of operation and 75,000 tonnes extracted.

In October 2022, SOMAIR, the Arlit uranium producer historically operated by French nuclear fuel company Orano, commissioned a new heap-leach area to process low-grade ore and extend the mine’s life.

However, political turmoil following the July 2023 coup disrupted chemical supplies and forced SOMAIR to halt yellowcake production in September 2023, although mining operations continued.

The disruption widened in 2024, when Niger withdrew Orano’s Imouraren permit in June and cancelled GoviEx’s Madaouela rights a month later, before entering talks with the Canadian miner on a revised framework for the project.

Niger has since intensified its overhaul of foreign mining agreements, including the military government’s nationalisation of SOMAIR in June 2025.

More recently, in May 2026, authorities cancelled a 58-year uranium concession linked to France at the strategic Arlit deposit.

The dispute has also drawn Russia into the sector, after Le Monde reported concern in France over a possible deal for Niger to sell about 1,000 tonnes of yellowcake to Rosatom for about $170 million, although Niger and Rosatom denied a confirmed agreement.

Consequently, Niger’s identified recoverable resources have also fallen, partly because of mining depletion and a lower estimate for Imouraren, while gains at Dasa and Takardeit only partly offset the decline.

South Africa remains a deep resource base

At the same time, South Africa remains one of Africa’s biggest uranium resource holders despite producing less than Namibia and Niger, and could become more important if stronger prices revive by-product and tailings projects.

Production was estimated at 192 tonnes in 2021 and 200 tonnes in 2022, with most historical output coming as a by-product of gold, or to a smaller extent copper from Palabora.

According to the Nuclear Energy Agency, current uranium production comes from Vaal River operations through reef material processed from Harmony Gold’s Moab Khotsong mine.

The Moab Khotsong underground mine, in northern South Africa, represents one of the country’s largest gold and uranium reserves, with total identified recoverable uranium resources of 8,360 tonnes.

Most uranium projects in South Africa are controlled by gold-mining companies, reflecting the country’s long history of producing uranium alongside precious metals.

France, China and Russia sharpen the race

France’s loss of influence in Niger has pushed Paris to reassess its African uranium supply routes, bringing Namibia, Botswana and Malawi into sharper focus as more stable alternatives.

At the same time, China’s control of key Namibian assets, including Husab and Rössing, has strengthened Beijing’s position in Africa’s uranium supply chain, while reported Russian interest in Nigerien uranium and Tanzania’s Mkuju River project has added another layer to the race for nuclear-fuel security.